Latin America Metal & Metallurgy Machinery Market (2026-2032) | Size, Companies, Share, Outlook, Revenue, Trends, COVID-19 IMPACT, Analysis, Industry, Growth, Value & Forecast

Market Forecast by Product Type (Metal rolling machinery, ironmaking equipment and steel making equipment), by Application (cutting, welding, non-metal processing, additive manufacturing and others), By Countries (Mexico, Brazil, Argentina, Chile and rest of Latin America) and Competitive Landscape

| Product Code: ETC054740 | Publication Date: Apr 2021 | Product Type: Report | ||

| Publisher: 6Wresearch | Author: Ravi Bhandari | No. of Pages: 200 | No. of Figures: 90 | No. of Tables: 30 |

Latin America Metal & Metallurgy Machinery Market Size, Share & Growth Rate

The Latin America Metal & Metallurgy Machinery Market was estimated at USD 376 Million in 2025 and is projected to reach USD 524 Million by 2032, growing at a CAGR of 4.9% from 2026 to 2032. This anticipated growth trajectory is primarily driven by the increasing demand from the aerospace and automotive sectors, where cutting-edge technologies are rapidly evolving. Additionally, government investments in infrastructure and the burgeoning renewable energy industry further augment this upward trend.

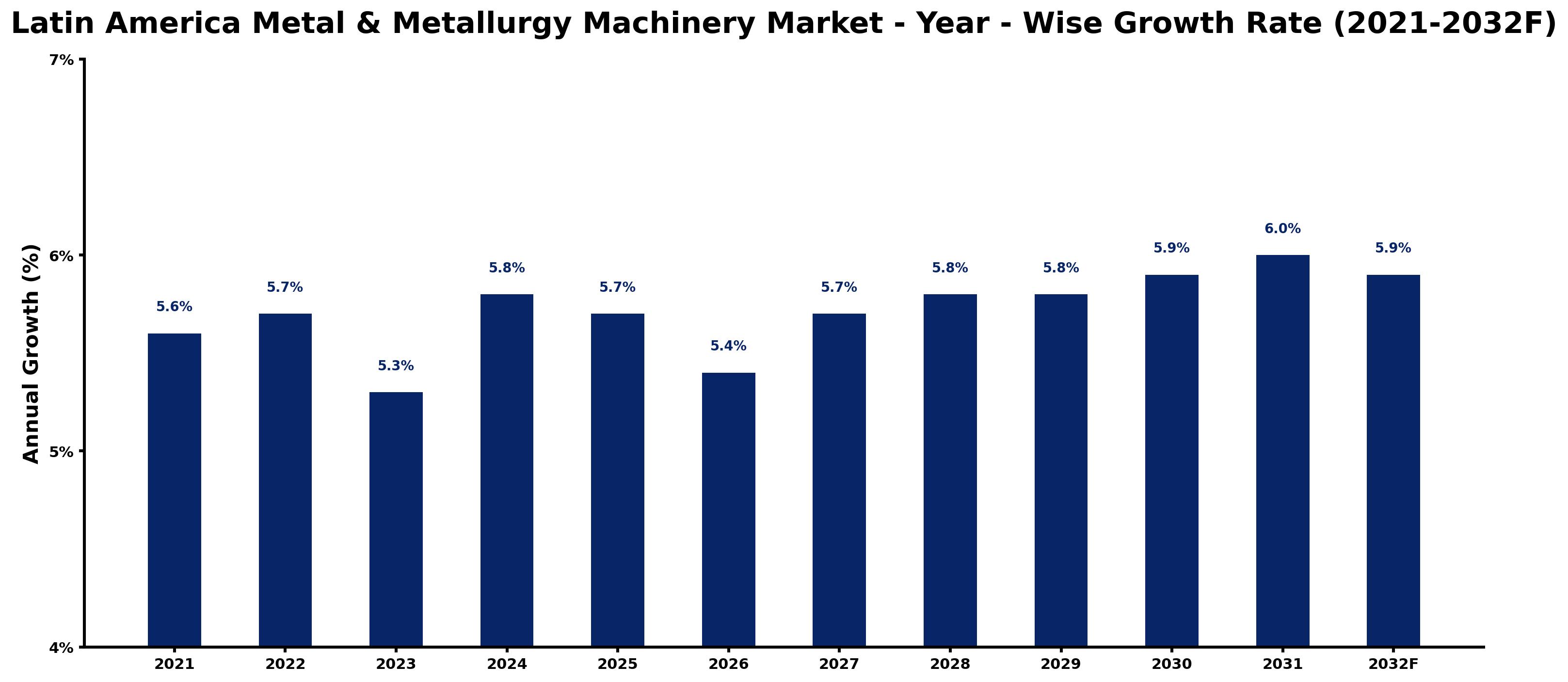

Latin America Metal & Metallurgy Machinery Market Year-wise Growth Rate and Key Drivers

This graph highlights how the Latin America Metal & Metallurgy Machinery Market has steadily grown over the years, supported by major growth factors.

The table below presents the year‑wise growth rates along with the key drivers influencing the market

| Year | Growth Rate | Major Drivers |

| 2021 | 5.6% | Expansion of manufacturing activities |

| 2022 | 5.7% | Increasing industrial automation investments |

| 2023 | 5.3% | Expansion of commercial construction activities |

| 2024 | 5.8% | Growing urbanization and commercial development |

| 2025 | 5.7% | Growing renewable energy integration projects |

| 2026 | 5.4% | Increasing industrial automation investments |

| 2027 | 5.7% | Rising electricity demand across industries |

| 2028 | 5.8% | Growing urbanization and commercial development |

| 2029 | 5.8% | Expansion of transportation and logistics networks |

| 2030 | 5.9% | Increasing industrial infrastructure investments |

| 2031 | 6.0% | Increasing adoption of advanced technologies |

| 2032 | 5.9% | Growing renewable energy integration projects |

Note - Market size estimations and growth projections presented in this report are based on 6Wresearch’s advanced forecasting approach, validated with industry datasets as of June 2026.

Latin America Metal & Metallurgy Machinery Market Synopsis

Recently, the Latin America Metal & Metallurgy machinery market experienced fluctuations due to the pandemic, which hampered industrial activities. However, as recovery sets in, the market is poised for robust growth, fueled by advancements in technology and rising investments in the aerospace and defense sectors. Companies are increasingly adopting innovative manufacturing practices, contributing to the market’s resilience and future potential.

Furthermore, the expansion of the consumer electronics market, supported by rising disposable incomes in the region, adds another layer of opportunity for machinery manufacturers. Countries like Brazil and Mexico are leading the charge, with sustained demand expected across various applications, particularly in cutting and welding technologies, which are critical for multiple industries.

Latin America Metal & Metallurgy Machinery Market Key Takeaways

- The market is projected to grow substantially from USD 376 Million in 2025 to USD 524 Million by 2032, reflecting a CAGR of 4.9%.

- Key drivers include strong demand from the aerospace, automotive, and consumer electronics sectors.

- Technological advancements and government expenditures are significant catalysts for growth.

- Brazil and Mexico dominate the market revenue share, with expected ongoing leadership during the forecast period.

- Investment in infrastructure and defense will continue to shape the market landscape positively.

Evaluation of Restraints in Latin America Metal & Metallurgy Machinery Market

While the Latin America Metal & Metallurgy Machinery Market is on a growth trajectory, several constraints impede its full potential. Economic volatility in the region, influenced by fluctuating commodity prices and currency instability, can impact industrial investments and consumer spending. Moreover, the pandemic has left lingering uncertainties, making stakeholders cautious in their long-term planning. Regulatory challenges and varying quality standards across countries further complicate market dynamics, potentially delaying project implementations and technological adoptions.

Latin America Metal & Metallurgy Machinery Market Trends

Current trends indicate a strong inclination towards automation and smart manufacturing technologies within the Metal & Metallurgy machinery space. The integration of IoT and AI technologies is enhancing productivity and operational efficiency, allowing manufacturers to streamline processes. Additionally, the adoption of additive manufacturing is gaining momentum, providing innovative solutions to traditional manufacturing challenges. Sustainability is also becoming a critical focus, with increasing efforts to reduce waste and improve energy efficiency in machinery operations.

Latin America Metal & Metallurgy Machinery Market Opportunities

The market presents significant opportunities for growth, particularly in expanding sectors such as renewable energy and electric vehicle manufacturing. As countries strive to enhance their energy mix and reduce carbon footprints, investments in advanced machinery that support these initiatives will likely rise. Furthermore, the increasing demand for localized production and nearshoring trends can propel investments in local manufacturing capabilities, benefiting the Metal & Metallurgy machinery sector.

Government Initiatives in the Latin America Metal & Metallurgy Machinery Market

Governments across Latin America are recognizing the importance of the Metal & Metallurgy sector as a pivotal driver of economic growth. Various public spending initiatives and policies aimed at bolstering infrastructure development are being introduced, with incentives for technology adoption and modernization of manufacturing processes. By fostering public-private partnerships and providing funding for research and development, authorities are paving the way for innovations that can bolster the industry's capabilities and competitiveness.

Future Insights of the Latin America Metal & Metallurgy Machinery Market

Looking ahead to the period from 2026 to 2032, the Latin America Metal & Metallurgy Machinery Market is set to evolve significantly. The ongoing digitization and automation of manufacturing processes are expected to drive new business models and enhance operational efficiencies. As the region's economies stabilize post-pandemic, sustained investments in key industries will likely contribute to a healthier market environment. The demand for advanced machinery will continue to rise, driven by the quest for innovation and the need for increased productivity in a competitive global landscape.

Latin America Metal & Metallurgy Machinery Market Latest Developments (May 2025 - June 2026)

In recent months, the industry has seen a resurgence in activity as companies adapt to the new market landscape. Innovations in machinery technology are being unveiled, showcasing improvements in efficiency and sustainability. Collaborative efforts between stakeholders are emerging, focusing on the development of more advanced manufacturing techniques. Furthermore, regional trade agreements and partnerships are beginning to pave the way for greater market accessibility, enhancing the potential for cross-border collaborations and technology transfers.

Latin America Metal & Metallurgy Machinery Market - Key Attractiveness of the Report

- 10 Years of Market Numbers

- Historical Data Starting from 2022 to 2025

- Base Year: 2025

- Forecast Data until 2032

- Key Performance Indicators Impacting the Market

- Major Upcoming Developments and Projects

Latin America Metal & Metallurgy Machinery Market - Frequently Asked Questions

The Latin America Metal & Metallurgy Machinery Market is estimated to be valued at USD 376 Million in 2025 and is projected to reach USD 524 Million by 2032, reflecting a CAGR of 4.9% from 2026 to 2032.

The push towards renewable energy is creating demand for advanced machinery that can support the production of cleaner technologies, thereby driving investments in the Metal & Metallurgy sector.

Government initiatives aimed at enhancing infrastructure and technological advancements are critical, providing financial incentives and regulatory frameworks that facilitate industry growth.

Brazil and Mexico stand out as key players, contributing significantly to market revenue and expected to maintain their dominance due to their robust industrial bases.

Automation and smart manufacturing technologies are at the forefront, with many players integrating IoT and AI to enhance operational efficiency and productivity.

6Wresearch actively monitors the Latin America Metal & Metallurgy Machinery Market and publishes its comprehensive annual report, highlighting emerging trends, growth drivers, revenue analysis, and forecast outlook. Our insights help businesses to make data-backed strategic decisions with ongoing market dynamics. Our analysts track relevent industries related to the Latin America Metal & Metallurgy Machinery Market, allowing our clients with actionable intelligence and reliable forecasts tailored to emerging regional needs.

Yes, we provide customisation as per your requirements. To learn more, feel free to contact us on sales@6wresearch.com

|

1. Executive Summary |

|

2. Introduction |

|

2.1. Key Highlights of the Report |

|

2.2. Report Description |

|

2.3. Market Scope & Segmentation |

|

2.4. Research Methodology |

|

2.5. Assumptions |

|

3. Latin America Metal & Metallurgy Market Overview |

|

3.1. Latin America Country Macro Economic Indicators |

|

3.2. Latin America Metal & Metallurgy Market Revenues, 2022 & 2032F |

|

3.3. Latin America Metal & Metallurgy Market - Industry Life Cycle |

|

3.4. Latin America Metal & Metallurgy Market - Porter's Five Forces |

|

3.5. Latin America Metal & Metallurgy Market Revenue Share, By Product Type, 2022 & 2032F |

|

3.6. Latin America Metal & Metallurgy Market Revenue Share, By Application, 2022 & 2032F |

|

4. Latin America Metal & Metallurgy Market Dynamics |

|

4.1. Impact Analysis |

|

4.2. Market Drivers |

|

4.3. Market Restraints |

|

5. Latin America Metal & Metallurgy Market Trends |

|

6. Latin America Metal & Metallurgy Market, By Product Type |

|

6.1. Latin America Metal & Metallurgy Market, By Product Type |

|

6.1.1. Overview and Analysis |

|

6.1.2. Latin America Metal & Metallurgy Market Revenues, By Metal Rolling Machinery, 2022-2032F |

|

6.1.3. Latin America Metal & Metallurgy Market Revenues, By Ironmaking Equipment, 2022-2032F |

|

6.1.4. Latin America Metal & Metallurgy Market Revenues, By Steelmaking Equipment, 2022-2032F |

|

6.2. Latin America Metal & Metallurgy Market, By Application |

|

6.2.1. Overview and Analysis |

|

6.2.2. Latin America Metal & Metallurgy Market Revenues, By Cutting, 2022-2032F |

|

6.2.3. Latin America Metal & Metallurgy Market Revenues, By Welding, 2022-2032F |

|

6.2.4. Latin America Metal & Metallurgy Market Revenues, By Non-metal Processing, 2022-2032F |

|

6.2.5. Latin America Metal & Metallurgy Market Revenues, By Additive Manufacturing, 2022-2032F |

|

6.2.6. Latin America Metal & Metallurgy Market Revenues, By Others, 2022-2032F |

|

7. Mexico Metal & Metallurgy Market |

|

7.1. Mexico Metal & Metallurgy Market, By Product Type |

|

7.1. Mexico Metal & Metallurgy Market, By Application |

|

7.1. Mexico Metal & Metallurgy Market, By Regions |

|

8. Chile Metal & Metallurgy Market |

|

8.1. Chile Metal & Metallurgy Market, By Product Type |

|

8.1. Chile Metal & Metallurgy Market, By Application |

|

8.1. Chile Metal & Metallurgy Market, By Regions |

|

9. Brazil Metal & Metallurgy Market |

|

9.1. Brazil Metal & Metallurgy Market, By Product Type |

|

9.1. Brazil Metal & Metallurgy Market, By Application |

|

9.1. Brazil Metal & Metallurgy Market, By Regions |

|

10. Argentina Metal & Metallurgy Market |

|

10.1. Argentina Metal & Metallurgy Market, By Product Type |

|

10.1. Argentina Metal & Metallurgy Market, By Application |

|

10.1. Argentina Metal & Metallurgy Market, By Regions |

|

11. Rest of Latin America Metal & Metallurgy Market |

|

11.1. Rest of Latin America Metal & Metallurgy Market, By Product Type |

|

12. Latin America Metal & Metallurgy Market Key Performance Indicators |

|

13. Latin America Metal & Metallurgy Market - Opportunity Assessment |

|

13.1. Latin America Metal & Metallurgy Market Opportunity Assessment, By Product Type, 2022 & 2032F |

|

13.2. Latin America Metal & Metallurgy Market Opportunity Assessment, By Application, 2022 & 2032F |

|

14. Latin America Metal & Metallurgy Market - Competitive Landscape |

|

14.1. Latin America Metal & Metallurgy Market Revenue Share, By Companies, 2025 |

|

14.2. Latin America Metal & Metallurgy Market Competitive Benchmarking, By Operating and Technical Parameters |

|

15. Company Profiles |

|

16. Recommendations |

|

17. Disclaimer |

Global Go To Market Strategy - 2030

Export potential enables firms to identify high-growth global markets with greater confidence by combining advanced trade intelligence with a structured quantitative methodology. The framework analyzes emerging demand trends and country-level import patterns while integrating macroeconomic and trade datasets such as GDP and population forecasts, bilateral import–export flows, tariff structures, elasticity differentials between developed and developing economies, geographic distance, and import demand projections. Using weighted trade values from 2020–2024 as the base period to project country-to-country export potential for 2030, these inputs are operationalized through calculated drivers such as gravity model parameters, tariff impact factors, and projected GDP per-capita growth. Through an analysis of hidden potentials, demand hotspots, and market conditions that are most favorable to success, this method enables firms to focus on target countries, maximize returns, and global expansion with data, backed by accuracy.

By factoring in the projected importer demand gap that is currently unmet and could be potential opportunity, it identifies the potential for the Exporter (Country) among 190 countries, against the general trade analysis, which identifies the biggest importer or exporter.

To discover high-growth global markets and optimize your business strategy:

Click Here

Pricing

- Single User License$ 4,560

- Department License$ 5,055

- Site License$ 5,595

- Global License$ 6,000

Leadership Perspectives from Industry Events

Search

Thought Leadership and Analyst Meet

Our Clients

6WResearch In News

- India Export Attractiveness Tracker 2026

- India Air Conditioner Market Set for Strong Rebound in 2026 After Weather-Led Correction and GST-Driven Recovery: 6Wresearch

- ADAS in India: How Automatic Emergency Braking, Blind Spot Detection & Driver Monitoring are Transforming Road Safety

- Doha a strategic location for EV manufacturing hub: IPA Qatar

- Demand for luxury TVs surging in the GCC, says Samsung

- Empowering Growth: The Thriving Journey of Bangladesh’s Cable Industry

Latest Reports

- Nicaragua RPG Gaming Market (2026-2032)

- New Zealand RPG Gaming Market (2026-2032)

- Netherlands RPG Gaming Market (2026-2032)

- Nauru RPG Gaming Market (2026-2032)

- Namibia RPG Gaming Market (2026-2032)

- Mozambique RPG Gaming Market (2026-2032)

- Montenegro RPG Gaming Market (2026-2032)

- Mongolia RPG Gaming Market (2026-2032)

- Monaco RPG Gaming Market (2026-2032)

- Micronesia RPG Gaming Market (2026-2032)

Industry Events and Analyst Meet

EV India Expo 2026

HIMTEX 2026

India Refining Summit 2026

India EV Show 2026

EV tech India Expo 2026

Whitepaper

- Middle East & Africa Commercial Security Market Click here to view more.

- Middle East & Africa Fire Safety Systems & Equipment Market Click here to view more.

- GCC Drone Market Click here to view more.

- Middle East Lighting Fixture Market Click here to view more.

- GCC Physical & Perimeter Security Market Click here to view more.