Vietnam 3D ICs Market (2026-2032) | Restraints, Demand, Competition, Competitive, Supply, Opportunities, Share, Strategy, Growth, Consumer Insights, Analysis, Segments, Forecast, Industry, Pricing Analysis, Outlook, Size, Segmentation, Strategic Insights, Trends, Drivers, Challenges, Revenue, Value, Companies, Investment Trends

Market Forecast By Technology (Through-Silicon Via, Package-on-Package), By Application (Memory, Imaging, Networking), By Manufacturing Process (Stacked, Monolithic), By End user (Automotive, Consumer Electronics) And Competitive Landscape

| Product Code: ETC11486516 | Publication Date: Apr 2025 | Updated Date: May 2026 | Product Type: Market Research Report | |

| Publisher: 6Wresearch | Author: Bhawna Singh | No. of Pages: 65 | No. of Figures: 34 | No. of Tables: 19 |

Vietnam 3D ICs Market Growth Rate

According to 6Wresearch internal database and industry insights, the Vietnam 3D ICs Market is estimated to grow at a compound annual growth rate (CAGR) of 16.4% during the forecast period (2026–2032).

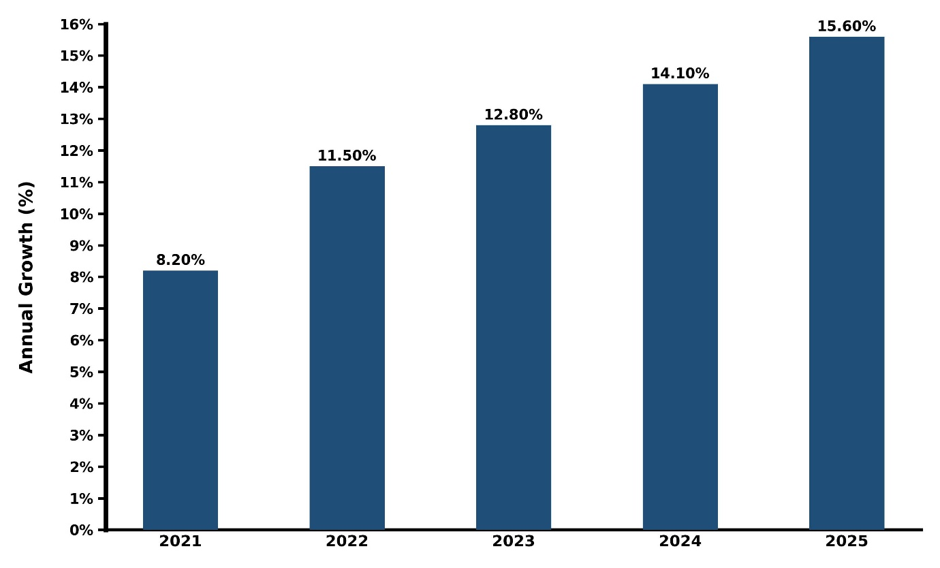

Vietnam 3D ICs Market Year-wise Growth Rate and Key Drivers

This graph highlights how the Vietnam 3D ICs Market has steadily grown over the past five years, supported by major growth factors.

Below is an evaluation of the year-wise growth rate along with foundational market drivers leading into the forecast period:

| Year | Est. Annual Growth (%) | Growth Drivers |

| 2021 | 8.2% | Expansion of testing facilities and legacy OSAT (Outsourced Semiconductor Assembly and Test) footprints in southern economic zones. |

| 2022 | 11.5% | Multinationals scaling up assembly lines and expanding foreign direct investment (FDI) into high-density electronic components. |

| 2023 | 12.8% | Shift toward localized sub-system packaging and structural policy shifts positioning Vietnam as a critical alternative supply chain hub in APAC. |

| 2024 | 14.1% | Smart investments by leading chip designing companies in the world and launch of powerful computing peripherals. |

| 2025 | 15.6% | Gigantic investments made in sophisticated testing facilities and achieving fundamental benchmarks for localizing backend integration networks |

Topics Covered in the Vietnam 3D ICs Market Report

The Vietnam 3D ICs Market report covers the market by technology, application, manufacturing process, and end user. The market report provides an unbiased and detailed analysis of ongoing market trends, opportunities, and drivers, which help stakeholders devise and align their market strategies according to the current and future market dynamics.

Vietnam 3D ICs Market Highlights

| Report Name |

Vietnam 3D ICs Market |

| Forecast period | 2026-2032 |

| CAGR | 16.4% |

| Market Size |

Semiconductor Advanced Packaging & Electronics Sector |

Vietnam 3D ICs Market Synopsis

The Vietnam 3D ICs Market is expanding as global supply chains shift toward Southeast Asia for advanced backend assembly, testing, and packaging (ATP). Driven by international foundry migrations and domestic technological targets, Vietnam is pivoting from legacy surface-mount operations to sophisticated multi-die architectural systems. A 3D IC is a chip architecture in which two or more semiconductor dies (chips) are placed on top of each other instead of side-by-side (2D layout) and interconnected using vertical electrical connections.

Evaluation of Growth Drivers in Vietnam 3D ICs Market (2026–2032)

Below are some major drivers and their influence on the market dynamics:

| Drivers | Primary Segment Affected | Why It Matters (Evidence) |

| Government Initiatives | Infrastructure, Fabrication Facilities | National strategies targeting specialized microelectronics training and foundational construction of chip manufacturing complexes in key high-tech parks. |

| Supply Chain Diversification | OSAT Centers, Substrate Assembly | Global technology giants redirecting capital into modern backend production nodes across dynamic provinces to achieve supply network resilience. |

| High-Performance Computing (HPC) | Memory Stacking, Interconnects | The regional rise in cloud data infrastructure and massive localized edge computing installations driving high-bandwidth requirements. |

| Consumer Electronics Hub Expansion | Package-on-Package (PoP), Mobile Logic | Expanding production lines for premium smartphones, tablets, and wearable sub-assemblies inside industrial corridors. |

| Automotive Electronics Modernization | In-Vehicle Infotainment, ADAS Sensors | Gradual upgrade of domestic smart electric vehicle production lines calling for compact, high-reliability stacked components. |

Vietnam 3D ICs Market is expected to continue its upward trajectory, exhibiting a CAGR of 16.4% during the forecast period (2026–2032), driven by rising investments in advanced semiconductor packaging, expansion of OSAT facilities, and increasing adoption of high-performance computing and AI-enabled chip architectures.

Vietnam 3D ICs market growth momentum is further supported by Vietnam’s strengthening position in the global electronics manufacturing ecosystem, where increasing foreign direct investment and supply chain diversification are accelerating the shift toward advanced technologies such as Through-Silicon Via (TSV) and system-in-package solutions.

Evaluation of Restraints in Vietnam 3D ICs Market

Below are some major restraints and their influence on the market dynamics:

| Restraints | Primary Segment Affected | What This Means (Evidence) |

| High Initial Cleanroom Capital Costs | Packaging Infrastructure, R&D Lines | Constructing extreme-precision thermocompression bonding facilities requires heavy initial cash outflows that squeeze localized ventures. |

| Workforce Specialization Gaps | Technical Engineering, Process Design | Shortages of advanced packaging process engineers trained in sub-micron vertical interconnect engineering can create onboarding bottlenecks. |

| Thermal Dissipation Complexities | High-Density Power Delivery, Logic Stacks | Stacking dies creates intense thermal-design-limit conditions that necessitate costly, custom advanced substrate structural materials. |

| Supply Substrate Dependencies | Advanced Silicon Interposers, Raw Materials | Continued reliance on external APAC heavyweights for high-end micro-vias and raw base wafers exposes lines to logistics friction. |

| Complex Yield Testing Cycles | Quality Inspection, Reliability Testing | Vertically integrated stacks present extreme cross-layer testing challenges, where a single structural defect ruins an entire multi-die package. |

Vietnam 3D ICs Market Challenges

Vietnam 3D ICs industry faces several structural and competitive challenges that may slow the pace of its advancement in the global semiconductor value chain. One of the most significant limitations is the limited domestic semiconductor design ecosystem, which restricts Vietnam’s ability to move up the value chain from assembly and packaging into high-value chip design and innovation.

Another problem is the dependence on foreign vendors of technologies essential for the 3D IC fabrication process. In essence, the technologies involved with the materials used, as well as packaging equipment and lithography, have to be imported, thus raising their cost and risk factor.

Vietnam 3D ICs Market Trends

Some of the key trends are:

- Proliferation of Heterogeneous System-in-Package (SiP) Implementations: The convergence of memory and logic components into modular packages is reshaping domestic production lines.

- Commercial Move Towards Glass and Panel-Level Substrates: Companies are looking into larger format panel-level packaging solutions in order to reduce costs associated with multi-die unit fabrication.

- Implementation of Machine Learning for Defect Detection in Cleanrooms: High-end test labs are employing machine learning algorithms for defect mapping of high-density integrated circuits.

Investment Opportunities in the Vietnam 3D ICs Market

Potential investment avenues available within the Vietnam 3D ICs Market are:

- Establishing High-Volume OSAT Facilities Focused on TSV Formats: Heavy investment opportunities lie in building fully operational third-party testing and assembly centers featuring modern vertical etching systems.

- Localized R&D Centers for Advanced Thermal Management Solutions: The development of thermal interface material designed to suit multi-die stacked packages opens up investment potential.

- Specialized Workforce Up-skilling Facilities and Tooling Institutes: Establishing microelectronics skill development ecosystems in conjunction with high-tech administrative districts provides profitable organizational investment options.

Top 5 Leading Players in Vietnam 3D ICs Market

Below are some of the leading companies operating in the Vietnam 3D ICs Market:

1. Samsung Electronics

| Company Name | Samsung Electronics |

|---|---|

| Established Year | Large-scale expansion since 2008 |

| Headquarters | Bac Ninh & Thai Nguyen, Vietnam |

| Official Website | Click Here |

Major electronics manufacturer involved in advanced semiconductor packaging for mobile and consumer devices, supporting global supply chains.

2. Intel Products

| Company Name | Intel Products |

|---|---|

| Established Year | 2006 |

| Headquarters | Ho Chi Minh City, Vietnam |

| Official Website | Click Here |

One of the largest semiconductor assembly and testing facilities globally, focusing on advanced packaging and microprocessor integration.

3. Amkor Technology Vietnam

| Company Name | Amkor Technology Vietnam |

|---|---|

| Established Year | 2023 expansion phase |

| Headquarters | Bac Ninh, Vietnam |

| Official Website | Click Here |

Leading OSAT provider specializing in advanced 3D IC packaging, flip-chip technology, and system-in-package solutions.

4. Foxconn Vietnam

| Company Name | Foxconn Vietnam |

|---|---|

| Established Year | 2007 |

| Headquarters | Bac Ninh, Vietnam |

| Official Website | Click Here |

Global electronics manufacturing company supporting semiconductor packaging and assembly for consumer electronics supply chains.

5. Renesas Electronics

| Company Name | Renesas Electronics |

|---|---|

| Established Year | 2002 |

| Headquarters | Tokyo, Japan (Vietnam operations present) |

| Official Website | Click Here |

Semiconductor design and solutions provider contributing to automotive and industrial chip integration and advanced IC development.

Government Initiatives Being Implemented in the Vietnam 3D ICs Market

The Vietnamese government has targeted advanced packaging and microelectronics as top-tier strategic industries. Specific actionable directives provide targeted relief to accelerate high-tech ecosystem maturation:

- Corporate Tax Exemptions: Companies within the National High-Tech Industrial Development Framework will enjoy a tax rate of 0% for 4 years of profit generation, and thereafter a cut in taxes by half for another 9 years.

- Hanoi and Ho Chi Minh Hi-Tech Park Subsidies: Projects that focus on genuine 3-D integration and Through Silicon Via (TSV) Lithography enjoy subsidies of 100% rental for land use while setting up their facilities in areas such as Hoa Lac Hi-Tech Park.

- National Semiconductor Talent Strategy 2030: An initiative to fund training of 50,000 semiconductors professionals who will be specifically used to build clean room laboratories for testing purposes.

Future Insights of the Vietnam 3D ICs Market

Vietnam 3D ICs market will be transformed into a leading semiconductor assembly hub, facilitated by foreign investments, policy coordination, and increasing international demand for advanced chip packaging technology. As the domestic ecosystem deepens, the integration line between front-end foundry fabrication and back-end packaging will continue to blur. Over the next decade, Vietnam’s manufacturing zones will transition from executing purely localized assembly towards driving complex architectural layout co-design. This maturation will establish the nation as an invaluable multi-die hub, supplying foundational sub-systems directly to international aerospace, communication, and processing hardware consortiums.

Market Segmentation Analysis

The report offers a comprehensive study of the following market segments and their leading categories:

By Technology - Through-Silicon Via (TSV) Dominates the Market

Through-Silicon Via (TSV) technology commands the dominant share of the market due to its unparalleled performance advantages in enabling high-density vertical electrical pathways. As TSVs pass directly through the silicon substrate, they create ultra-short interconnect lengths that minimize latency and vastly reduce power consumption compared to older side-by-side alternatives.

By Application - Memory Leads the Market

According to Parth, Senior Research Analyst, 6Wresearch, the memory category represents the highest volume segment within the domestic production landscape, driven primarily by the global shift toward High-Bandwidth Memory (HBM) architectures and dense 3D NAND vertical arrays. High-performance computing systems and AI accelerator nodes demand exceptional data access speeds that conventional memory designs can no longer sustain.

By Manufacturing Process - Stacked 3D To Lead the Market

Stacked 3D processing holds a dominant position across active manufacturing pipelines due to it leverages mature, highly reliable die-to-die and die-to-wafer bonding techniques. This methodology allows separate, pre-tested functional elements to be physically arranged on top of each other, keeping fabrication lines highly flexible.

By End User - Consumer Electronics Dominates the Market

Consumer electronics are expected to lead the Vietnam 3D ICs market share, spurred by the continuous demand for smaller, more power-efficient mobile handsets, wearable monitors, and high-tier computing gadgets. Device makers are continually forced to squeeze multi-functional chip architectures into extremely thin, lightweight product form factors.

Key Attractiveness of the Report:

- 10 Years of Market Numbers

- Historical Data Starting from 2022 to 2025

- Base Year: 2025

- Forecast Data until 2032

- Key Performance Indicators Impacting the Market

- Major Upcoming Developments and Projects

Key Highlights of the Report:

- Vietnam 3D Ics Market Outlook

- Market Size of Vietnam 3D Ics Market, 2025

- Forecast of Vietnam 3D Ics Market, 2032

- Historical Data and Forecast of Vietnam 3D Ics Revenues & Volume for the Period 2022 - 2032

- Vietnam 3D Ics Market Trend Evolution

- Vietnam 3D Ics Market Drivers and Challenges

- Vietnam 3D Ics Price Trends

- Vietnam 3D Ics Porter's Five Forces

- Vietnam 3D Ics Industry Life Cycle

- Historical Data and Forecast of Vietnam 3D Ics Market Revenues & Volume By Technology for the Period 2022 - 2032

- Historical Data and Forecast of Vietnam 3D Ics Market Revenues & Volume By Through-Silicon Via for the Period 2022 - 2032

- Historical Data and Forecast of Vietnam 3D Ics Market Revenues & Volume By Package-on-Package for the Period 2022 - 2032

- Historical Data and Forecast of Vietnam 3D Ics Market Revenues & Volume By Application for the Period 2022 - 2032

- Historical Data and Forecast of Vietnam 3D Ics Market Revenues & Volume By Memory for the Period 2022 - 2032

- Historical Data and Forecast of Vietnam 3D Ics Market Revenues & Volume By Imaging for the Period 2022 - 2032

- Historical Data and Forecast of Vietnam 3D Ics Market Revenues & Volume By Networking for the Period 2022 - 2032

- Historical Data and Forecast of Vietnam 3D Ics Market Revenues & Volume By Manufacturing Process for the Period 2022 - 2032

- Historical Data and Forecast of Vietnam 3D Ics Market Revenues & Volume By Stacked for the Period 2022 - 2032

- Historical Data and Forecast of Vietnam 3D Ics Market Revenues & Volume By Monolithic for the Period 2022 - 2032

- Historical Data and Forecast of Vietnam 3D Ics Market Revenues & Volume By End user for the Period 2022 - 2032

- Historical Data and Forecast of Vietnam 3D Ics Market Revenues & Volume By Automotive for the Period 2022 - 2032

- Historical Data and Forecast of Vietnam 3D Ics Market Revenues & Volume By Consumer Electronics for the Period 2022 - 2032

- Vietnam 3D Ics Import Export Trade Statistics

- Market Opportunity Assessment By Technology

- Market Opportunity Assessment By Application

- Market Opportunity Assessment By Manufacturing Process

- Market Opportunity Assessment By End user

- Vietnam 3D Ics Top Companies Market Share

- Vietnam 3D Ics Competitive Benchmarking By Technical and Operational Parameters

- Vietnam 3D Ics Company Profiles

- Vietnam 3D Ics Key Strategic Recommendations

Market Covered

The report offers an extensive study of the following market segments:

By Technology

- Through-Silicon Via (TSV)

- Package-on-Package (PoP)

By Application

- Memory

- Imaging

- Networking

By Manufacturing Process

- Stacked

- Monolithic

By End User

- Automotive

- Consumer Electronics

Vietnam 3D ICs Market (2026-2032): FAQs

Vietnam 3D ICs Market is anticipated to grow at a compound annual growth rate (CAGR) of 16.4% during the forecast period (2026-2032).

Some primary drivers include supply chain diversification, government semiconductor initiatives, rising electronics manufacturing, and increasing AI adoption.

Consumer Electronics segment currently generates the highest baseline order volumes, driven by the regional manufacture of mobile communication processing blocks.

Some major challenges include high capital investment, skilled workforce shortage, and dependency on imported semiconductor equipment.

6Wresearch actively monitors the Vietnam 3D ICs Market and publishes its comprehensive annual report, highlighting emerging trends, growth drivers, revenue analysis, and forecast outlook. Our insights help businesses to make data-backed strategic decisions with ongoing market dynamics. Our analysts track relevent industries related to the Vietnam 3D ICs Market, allowing our clients with actionable intelligence and reliable forecasts tailored to emerging regional needs.

Yes, we provide customisation as per your requirements. To learn more, feel free to contact us on sales@6wresearch.com

| 1 Executive Summary |

| 2 Introduction |

| 2.1 Key Highlights of the Report |

| 2.2 Report Description |

| 2.3 Market Scope & Segmentation |

| 2.4 Research Methodology |

| 2.5 Assumptions |

| 3 Vietnam 3D Ics Market Overview |

| 3.1 Vietnam Country Macro Economic Indicators |

| 3.2 Vietnam 3D Ics Market Revenues & Volume, 2022 & 2032F |

| 3.3 Vietnam 3D Ics Market - Industry Life Cycle |

| 3.4 Vietnam 3D Ics Market - Porter's Five Forces |

| 3.5 Vietnam 3D Ics Market Revenues & Volume Share, By Technology, 2022 & 2032F |

| 3.6 Vietnam 3D Ics Market Revenues & Volume Share, By Application, 2022 & 2032F |

| 3.7 Vietnam 3D Ics Market Revenues & Volume Share, By Manufacturing Process, 2022 & 2032F |

| 3.8 Vietnam 3D Ics Market Revenues & Volume Share, By End user, 2022 & 2032F |

| 4 Vietnam 3D Ics Market Dynamics |

| 4.1 Impact Analysis |

| 4.2 Market Drivers |

| 4.2.1 Growing demand for high-performance electronic devices in Vietnam |

| 4.2.2 Increasing adoption of Internet of Things (IoT) devices and smart technologies |

| 4.2.3 Government initiatives to support the development of the semiconductor industry in Vietnam |

| 4.3 Market Restraints |

| 4.3.1 Limited technological infrastructure and expertise for 3D ICs manufacturing in Vietnam |

| 4.3.2 High initial investment and production costs associated with 3D IC technology |

| 4.3.3 Lack of standardized regulations and guidelines for 3D ICs in Vietnam |

| 5 Vietnam 3D Ics Market Trends |

| 6 Vietnam 3D Ics Market, By Types |

| 6.1 Vietnam 3D Ics Market, By Technology |

| 6.1.1 Overview and Analysis |

| 6.1.2 Vietnam 3D Ics Market Revenues & Volume, By Technology, 2022 - 2032F |

| 6.1.3 Vietnam 3D Ics Market Revenues & Volume, By Through-Silicon Via, 2022 - 2032F |

| 6.1.4 Vietnam 3D Ics Market Revenues & Volume, By Package-on-Package, 2022 - 2032F |

| 6.2 Vietnam 3D Ics Market, By Application |

| 6.2.1 Overview and Analysis |

| 6.2.2 Vietnam 3D Ics Market Revenues & Volume, By Memory, 2022 - 2032F |

| 6.2.3 Vietnam 3D Ics Market Revenues & Volume, By Imaging, 2022 - 2032F |

| 6.2.4 Vietnam 3D Ics Market Revenues & Volume, By Networking, 2022 - 2032F |

| 6.3 Vietnam 3D Ics Market, By Manufacturing Process |

| 6.3.1 Overview and Analysis |

| 6.3.2 Vietnam 3D Ics Market Revenues & Volume, By Stacked, 2022 - 2032F |

| 6.3.3 Vietnam 3D Ics Market Revenues & Volume, By Monolithic, 2022 - 2032F |

| 6.4 Vietnam 3D Ics Market, By End user |

| 6.4.1 Overview and Analysis |

| 6.4.2 Vietnam 3D Ics Market Revenues & Volume, By Automotive, 2022 - 2032F |

| 6.4.3 Vietnam 3D Ics Market Revenues & Volume, By Consumer Electronics, 2022 - 2032F |

| 7 Vietnam 3D Ics Market Import-Export Trade Statistics |

| 7.1 Vietnam 3D Ics Market Export to Major Countries |

| 7.2 Vietnam 3D Ics Market Imports from Major Countries |

| 8 Vietnam 3D Ics Market Key Performance Indicators |

| 8.1 Research and development investment in 3D IC technology in Vietnam |

| 8.2 Number of partnerships and collaborations between local and international semiconductor companies |

| 8.3 Adoption rate of 3D IC technology in key industries in Vietnam |

| 9 Vietnam 3D Ics Market - Opportunity Assessment |

| 9.1 Vietnam 3D Ics Market Opportunity Assessment, By Technology, 2022 & 2032F |

| 9.2 Vietnam 3D Ics Market Opportunity Assessment, By Application, 2022 & 2032F |

| 9.3 Vietnam 3D Ics Market Opportunity Assessment, By Manufacturing Process, 2022 & 2032F |

| 9.4 Vietnam 3D Ics Market Opportunity Assessment, By End user, 2022 & 2032F |

| 10 Vietnam 3D Ics Market - Competitive Landscape |

| 10.1 Vietnam 3D Ics Market Revenue Share, By Companies, 2025 |

| 10.2 Vietnam 3D Ics Market Competitive Benchmarking, By Operating and Technical Parameters |

| 11 Company Profiles |

| 12 Recommendations |

| 13 Disclaimer |

Global Go To Market Strategy - 2030

Export potential enables firms to identify high-growth global markets with greater confidence by combining advanced trade intelligence with a structured quantitative methodology. The framework analyzes emerging demand trends and country-level import patterns while integrating macroeconomic and trade datasets such as GDP and population forecasts, bilateral import–export flows, tariff structures, elasticity differentials between developed and developing economies, geographic distance, and import demand projections. Using weighted trade values from 2020–2024 as the base period to project country-to-country export potential for 2030, these inputs are operationalized through calculated drivers such as gravity model parameters, tariff impact factors, and projected GDP per-capita growth. Through an analysis of hidden potentials, demand hotspots, and market conditions that are most favorable to success, this method enables firms to focus on target countries, maximize returns, and global expansion with data, backed by accuracy.

By factoring in the projected importer demand gap that is currently unmet and could be potential opportunity, it identifies the potential for the Exporter (Country) among 190 countries, against the general trade analysis, which identifies the biggest importer or exporter.

To discover high-growth global markets and optimize your business strategy:

Click Here

Pricing

- Single User License$ 1,995

- Department License$ 2,400

- Site License$ 3,120

- Global License$ 3,795

Leadership Perspectives from Industry Events

Search

Thought Leadership and Analyst Meet

Our Clients

6WResearch In News

- Doha a strategic location for EV manufacturing hub: IPA Qatar

- Demand for luxury TVs surging in the GCC, says Samsung

- Empowering Growth: The Thriving Journey of Bangladesh’s Cable Industry

- Demand for luxury TVs surging in the GCC, says Samsung

- Video call with a traditional healer? Once unthinkable, it’s now common in South Africa

- Intelligent Buildings To Smooth GCC’s Path To Net Zero

Latest Reports

- Poland Fire Protection Systems Market (2026-2032)

- Cape Verde Portable Hand-Thrown Extinguisher Market (2026-2032)

- Canada Portable Hand-Thrown Extinguisher Market (2026-2032)

- Cameroon Portable Hand-Thrown Extinguisher Market (2026-2032)

- Burundi Portable Hand-Thrown Extinguisher Market (2026-2032)

- Burkina Faso Portable Hand-Thrown Extinguisher Market (2026-2032)

- Bulgaria Portable Hand-Thrown Extinguisher Market (2026-2032)

- Brunei Portable Hand-Thrown Extinguisher Market (2026-2032)

- Botswana Portable Hand-Thrown Extinguisher Market (2026-2032)

- Bosnia and Herzegovina Portable Hand-Thrown Extinguisher Market (2026-2032)

Industry Events and Analyst Meet

HIMTEX 2026

India Refining Summit 2026

India EV Show 2026

EV tech India Expo 2026

Auto Tech Asia 2026

Whitepaper

- Middle East & Africa Commercial Security Market Click here to view more.

- Middle East & Africa Fire Safety Systems & Equipment Market Click here to view more.

- GCC Drone Market Click here to view more.

- Middle East Lighting Fixture Market Click here to view more.

- GCC Physical & Perimeter Security Market Click here to view more.